Cyclicity and Tests for Stationarity¶

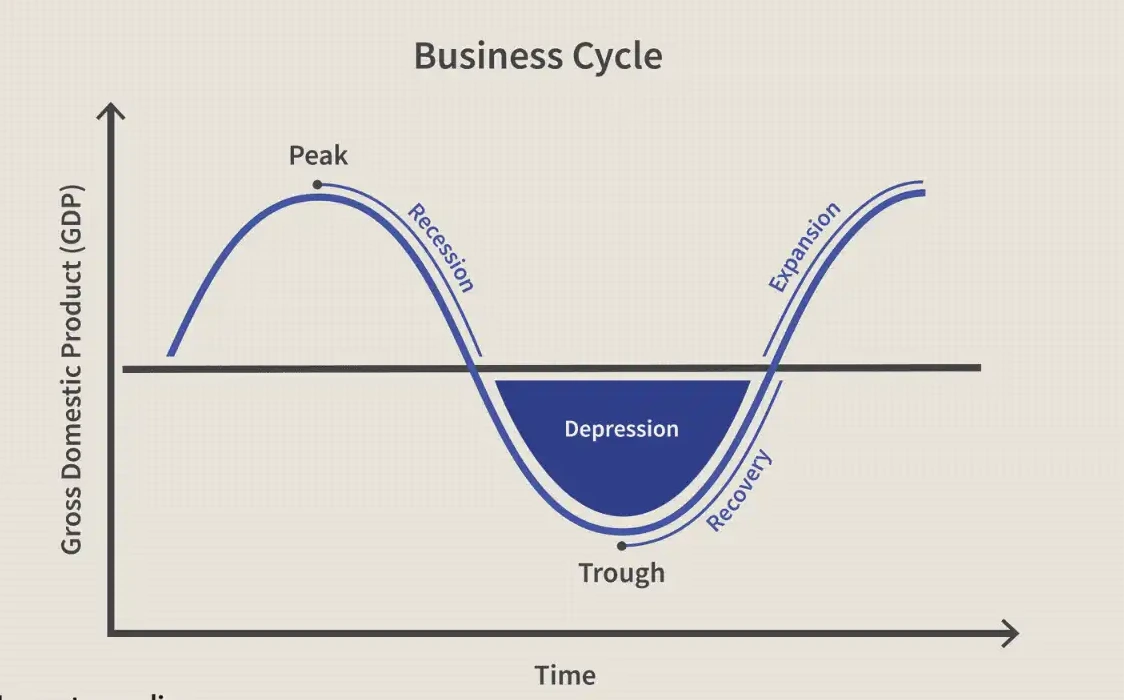

1. Cyclical Variations¶

Cyclicality refers to gradual, long-term, and irregular repetitive movements in a time series. Unlike seasonality, these fluctuations do not have a fixed frequency, and the period usually extends beyond a single year.

The 6 Phases of a Business Cycle:

- Expansion

- Peak

- Recession

- Depression

- Trough

- Recovery

Examples:

* Business Cycles: Periodic economic growth and contraction.

* Price Cycles: Influenced by production decisions and supply-demand lags.

* Solar Cycles: Every 11 years, the Sun's magnetic poles shift entirely, impacting solar activity.

2. Seasonality vs. Cyclicality¶

| Feature | Seasonality | Cyclicality |

|---|---|---|

| Origin | Calendar Effects | Irregular fluctuations |

| Frequency | Fixed frequency | No fixed frequency |

| Length | Average length is smaller (\(\le 1\) year) | Usually longer than 1 year |

| Magnitude | Generally lower magnitude | Magnitude of cycles is higher |

3. Unit Roots and Non-Stationarity¶

A unit root exists when one of the characteristic roots of the model equation is equal to 1.

Unit Root Impact

Unit roots make a process non-stationary because the model will never converge to a constant mean.

Example:

Consider the model: \(Y_{t} - 1.9 Y_{t-1} + 0.9 Y_{t-2} = e_{t} - 0.5 e_{t-1}\).

This can be rewritten using the backshift operator as: \((1 - 1.9B + 0.9B^{2}) Y_{t} = (1 - B)(1 - 0.9B)Y_{t}\).

The roots are \(1\) and \(\frac{10}{9}\). Because of the unit root (\(1\)), the original model is an \(ARIMA(1,1,1)\) and is non-stationary. Once differenced (\(W_t = \nabla Y_t\)), it becomes a stationary \(ARMA(1,1)\).

Why are Unit Roots a problem?

A unit root implies the structure \((1-B)Y_{t} = f(e_{t})\), or \(Y_{t} = Y_{t-1} + f(e_{t})\). This means the current value is simply the past value plus some random error. Consequently, the variance grows over time, and the series does not return to a long-run mean.

4. Tests of Stationarity¶

Statistical tests help determine if a series is stationary or if transformations are needed.

Augmented Dickey-Fuller (ADF) Test¶

This test checks for the presence of a unit root.

* \(H_{0}\): Series is non-stationary (Unit root exists).

* \(H_{a}\): Series is stationary.

Kwiatkowski-Phillips-Schmidt-Shin (KPSS) Test¶

This test checks for a deterministic trend or mean stationarity. Unlike the ADF, the null hypothesis is stationarity.

* \(H_{0}\): Series is stationary.

* \(H_{a}\): Series is non-stationary.

Phillips-Perron (PP) Test¶

The PP test shares the same goal and hypothesis setup as the ADF test but uses different assumptions about error terms.

* Robustness: It is more robust in the presence of autocorrelation and heteroskedasticity.

Variance Ratio Test¶

This is a specific test for a random walk.

* \(H_{0}\): Series is non-stationary.

* \(H_{a}\): Series is stationary.

* Logic: If the calculated ratio is significantly different from \(1\), the series is not a random walk.