Sahasrabuddhe: Development in Layers

Study Strategy¶

- The source material is daunting, and unnecessarily rigorous. I feel start basic and once you have grasped the mechanism of adjustments, then go for the source material (optional)

- Solve questions and work your way back to theory to stitch everything together!

- First learn how to calculate the trend indices, and practice.

- Claim Size model will require you to refer back to material.

- Calculate LEV depending on distribution, formula given on the exam

- \(L(d,p)\) for a layer is just difference

Big Picture¶

- We have ultimate claim size mean → adjust it for trends then you have it for every cell → use these to find limited expected values in a layer and relativities between layers \(a\) and \(b\).

- \(a\) = Basic limit; \(b\) = Limits of our given table

- Use relativities to calculate cumulative triangles at current year cost levels and basic limits → Denominator = current @ original limits, Numerator = latest @ basic limits

- Calculate LDFs from this Adjusted Cumulative triangle

Checklist¶

- Be able to explain why we need to adjust loss development factors in different layers

- Be able to calculate the trend index

- Be able to calculate LEVs given values of \(\theta\) and the LEV formula for a distribution

- Be able to calculate adjusted loss development factors for a given layer

- Adjust the cumulative losses to the basic limit and appropriate cost level

- Calculate the LDFs based on the adjusted cumulative losses

- Use the LEVs to adjust the LDFs for the given layer

- Be able to explain the impact the value of theta has on the adjusted LDFs

- Be able to describe the purpose of a claims layer ratio

- Know the properties of the claims layer ratio

- Be able to calculate adjusted LDFs using the claims layer ratio and the LEVs at ultimate

My Notes¶

The point

Adjust LDF for one claim layer to produce LDFs appropriate for another layer.

- Useful for high deductible and XOL reinsurance policies (with thinness in excess/ceded layer)

Notation¶

- Exposure period (AY) \(i\)

- Development period \(j\)

- \(C^L_{i,j}\) → Cumulative claims in \(L\)

- \(C_{i,\infty}^L\) → Ultimate claims in \(L\)

- \(f_{n,j}^L\) → Age-to-age (LDF)

- \(F^L_{n,j}\) → Age-to-ult (CDF)

- \(L(d,p)\) → claims layer (\(0 \leq d < p \leq \infty\))

- truncated below \(d\) → deductible

- censored above \(p\) → policy limit

- \(d=0, p=\infty\) → ground-up unlimited basis

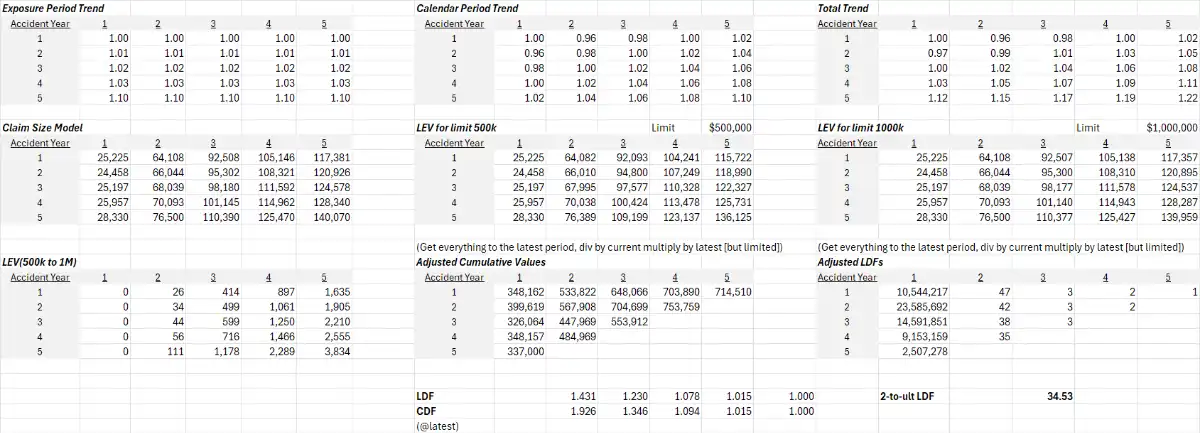

Trend¶

- Trends apply to and are calculated from ground-up unlimited claims layer

Complication about selection of trend factors

- Trend typically acts on incremental values

- Analysis uses cumulative data

- Then exactly what trend factors to apply to this data?

Steps¶

- Calculate AY trend (row-wise)

- Calculate CY trend (diagonally)

- Total trend = AY \(\times\) CY (for \(T_{ij}\) values)

Claim Size Model¶

- Calculate LEVs from the distribution → Every distribution has a limited version, in Exam P, we had seen this as \(E(X \wedge L)\) and is provided in the tables for each distribution. Each cell has a mean value which can be used to determine it. We will typically be given the exponential distribution.1

- \(LEV(L(d,p)) = LEV(p) - LEV(d)\) for a given distribution \(\Phi\)

How \(\theta\) impacts adjusted LDFs

- If claim size parameters (\(\theta\)'s) are larger

- adjustment of LDFs below limit is impactful ← Greater difference between adjusted and unadjusted factors

- the impact from a larger trend would be the same.

- If \(\theta\)'s are smaller (less claims are being censored at policy limit)

- limited LEVs are closer to unlimited LEVs

- Adjustment of LDFs below limit is less impactful (← difference between adjusted and unadjusted factors is minimal)

- but above the limit is more impactful (← fewer losses in excess layer)

Adjusting LDFs¶

Why adjust LDFs?

- Traditional Chain Ladder to calculate LDFs is appropriate if our loss data

- is on a ground-up (\(d=0\))

- unlimited basis (\(p = \infty\))

- and trend only acts in AY direction

- If either of these aren't true \(\implies\) We need to adjust LDFs

Use 500k as Basic limit unless told otherwise

- Basic limit = data is sufficiently credible for estimating claims development patterns

- To adjust LDFs

- Adjust Original loss triangle to latest period's cost level @ basic limit

- Use \(\uparrow\) to calculate LDFs → CDFs

- Adjust CDFs for any layer

Let's look at how to do the last step. For layer \(X\)

\[

F_{ij}^X = F_{n,j}^B \times \dfrac{\text{Ult in Layer}/\text{Ult Latest Basic}}{\text{Dev(j) in Layer}/\text{Dev(j) Latest Basic}}

\]

- Its best to create an "in Layer" table (using the relation \(LEV(L(d,p)) = LEV(p) - LEV(d)\))

- And apply this adjustment to CDFs \(= \dfrac{\text{Ult in Layer}}{\text{Dev(j) in Layer}} / \dfrac{\text{Ult Latest Basic}}{\text{Dev(j) Latest Basic}}\)

- So, to remember, you are calculating \(\dfrac{\text{CDF for Layer}}{\text{CDF for Basic @Latest}}\) and multiplying it to selected CDFs from Basic @Latest

Claims Layer Ratios¶

The Goal

Find LDFs for

- There is no claim size model for maturities other than ultimate.

- But don't try to develop one. Just estimate the ratios

\[

\text{Claims Layer Ratio} = R_{j}(B,X) = \dfrac{LEV(B)}{LEV(X)}

\]

- Adjustment factors for for LDFs

- Basic \(=\dfrac{\text{LEV(Basic, Ult)}}{\text{LEV(Limited, Ult)}}/\text{Claims Layer Ratio}\)

- Basic → Limit (X) \(=\left(1-\dfrac{\text{LEV(Basic, Ult)}}{\text{LEV(Limited, Ult)}}\right)/(1-\text{Claims Layer Ratio})\)

Properties of Claims Layer Ratio

For \(R_{j}(B,X) \lt 1\) (i.e. ignoring negative dev for which it would be \(\geq 1\))

- \(R_{a} \gt R_{b}\) (\(a < b\)) for earlier maturities → less development in excess layer earlier on. (e.g. \(R_{12} \gt R_{24}\))

- \(R_{a} \geq R_{\infty}\) → Pre-mature (reported) ratios will be greater than ultimate \(\impliedby\) more development in higher layers than lower layers2

- If LDFs calculated from unlimited data → \(\max{R} = R_{\infty} \times F_{j}\) #doubt