Measuring the Variability of Chain Ladder Reserve Estimates - Mack (1994)

Study Strategy¶

This paper has a lot of stuff that you have to memorize, but instead of memorizing stuff one by one. I suggest you do it as a whole. Get the context which makes individual components easy to remember.

- The scope of these paper includes:

- Mack's 3 assumptions (Totally 4 since, assumption #1 has two parts), and how to verify them?

- For different variance assumptions, which LDFs \(f_{k}\) to use?

- Calculating variance of chain ladder estimates (TAKE YOUR TIME HERE)

- Follow the checklist. In particular, these are the things you have to do:

- Assumption #1, #1i, #2, #3 have tests. #1i and #2 are methodical and you should practice them with examples to get a hang of it instead of trying to memorize anything. Get into the sheets directly (TWSS).

- Calculating variance involves multiple steps but it is actually pretty easy to do. There is a #Master Table which tells you exactly what all you need to calculate.

- Just finish through all the problems (would take you around 1 day to do, but take your time)

Checklist¶

- Be able to list the three chain ladder assumptions

- Know the three different variance assumptions, and how to calculate \(f_k\) under each assumption

- Be able to perform the different assumption tests, know if the data passes or fails the test, and know what assumption it’s testing:

- Calendar year effects test

- Regression test

- Spearman’s rank test

- Residual plot test

- Be able to calculate the confidence interval for individual accident years:

- Know why we prefer a lognormal distribution rather than a normal distribution

- Calculate \(\alpha^2\)

- Calculate the standard error of the individual reserves

- Calculate the variance, \(\sigma^2\)

- Be able to calculate an empirical confidence interval

My Notes¶

Notation¶

- \(f_{k}:\) age-to-age factors

- \(R_{i}:\) reserves

- \(I:\) # of AYs

- \(I-k\) refers to the number of cells in the columns for \(k\) in an LDF triangle.

Assumptions¶

- #1: Expected cum losses in the next dev period are proportional to losses to date

- #1i: Development factors are uncorrelated

- #2: Losses in one AY are independent of losses in another AY

- #3: Variance of cumulative losses in next period are proportional to losses reported to date

- \(E(C_{i,k+1}|C_{i1}, \dots, C_{ik}) = C_{ik}f_{k}\)

- \(\implies\) Dev factors \(f_{k-1},f_{k},f_{k+1}\) are uncorrelated

- Assumption doesn't hold if correlated → An unusually low dev factor immediately following an unusually high dev factor

- Accident years are independent.

- Violated by Calendar year effects → major changes in claims handling or case

- \(Var(C_{i,k+1}| C_{i 1},\dots, C_{i k}) = C_{ik} \alpha_{k}^{2}\)

- \(\alpha_{k}^{2}\) = unknown constant

| Variance Assumptions | Dev factor, \(f_{k} =\) | Plain English |

|---|---|---|

| \(Var(C_{i,K+1} \|\cdot)= \alpha_{k}^{2}\) | \(\dfrac{\sum_{i=1}^{I-k}C_{ik}^{2}f_{ik}}{\sum_{i=1}^{I-k}C_{ik}^{2}}\) | Constant variance, weight by \(C^2\) |

| \(Var(C_{i,K+1}\|\cdot) = C_{ik}\alpha^{2}_{k}\) | \(\dfrac{\sum_{i=1}^{I-k}C_{ik}f_{ik}}{\sum_{i=1}^{I-k}C_{ik}}\) | Mack's case, weight by volume |

| \(Var(C_{i,K+1} \|\cdot)= C_{ik}^{2}\alpha_{k}^{2}\) | \(\dfrac{\sum_{i=1}^{I-k}f_{ik}}{I - k}\) | Var prop to \(C^{2}\), simple average |

Tests¶

The name of the test and the associated (Assumption #) being tested.

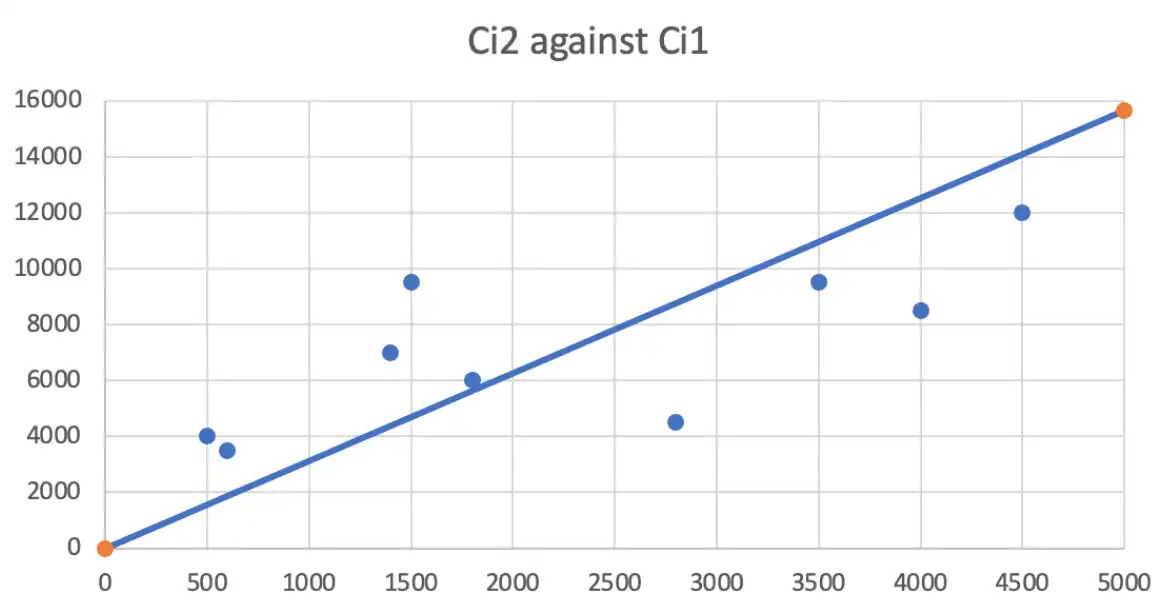

Regression Test (#1)¶

- Plot \(C_{i,k+1}\) against \(C_{ik}\) for every development period \(k\).

- Check if it approximately linear relationship around \(y=f_{k}\).

- Underestimate losses less than 2000 and overestimate otherwise

- Mack suggest → Do a regression with an additional intercept parameter

- If all pairings past the test, the dataset passes the test.

Spearman's rank Test (#1i1)¶

KEYWORD = 'rank', which means we have to the

=rankfunction ;)

- Distribution free test for independence

- Look at triangle as a whole (rather than individual pairs)

Looking at the whole triangle

- Lets us know if correlation prevails globally than in a small part of the triangle.

- Helps avoid an accumulation of error probabilities

Steps¶

- Calculate LDFs

- Rank the LDFs for each pair of factors

=rank(D1,D1:D3,1)

| \(s_{i 2}\) | \(r_{i 2}\) | \(s_{i 3}\) | \(r_{i 3}\) | |

|---|---|---|---|---|

| \(i=1\) | 2 | 1 | 1 | 2 |

| \(i=2\) | 3 | 2 | 2 | 1 |

| \(i=3\) | 1 | 3 |

- Calculate \((r_{ik}- s_{ik})^{2}\) → sum column \(S_{k}\)

| \(k=2\) | \(k=3\) | |

|---|---|---|

| \(i=1\) | 1 | 1 |

| \(i=2\) | 1 | 1 |

| \(i=3\) | \(2^2=4\) |

- Let \(n\) be the number of Rank-pairs in column

- \(T_{k} = 1 - 6 \dfrac{S_{k}}{n(n^{2}-1)}\)

- \(T\) = Weighted average of \(T_{k}\) with \((\#AY-k-1)\) as weights

| \(k\) | 2 | 3 |

|---|---|---|

| \(T_{k}\) | -0.5 | 1 |

| \(\text{weight}_{k}\) | 2 | 1 |

- \(E(T)= 0\) and \(Var(T) = \dfrac{1}{(\text{\#AY}-2)(\text{\# AY}-3)/2}\)

- C.I. = \(0 \pm z \sqrt{ Var(T) }\)

Calendar Year Effects test (#2)¶

Reasons for calendar year effects

- Internal

- Strengthening of case reserves

- Changes in claim settlement rates

- External

- Legislative or legal changes

- Greater than average inflation

We fail to prove that there are significant calendar events.

Steps¶

- Calculate LDFs

- Calculate median

- \(S\) → Smaller than median

- \(*\) → equal to median

- \(L\) → larger than median

- Count \(L\)'s and \(S\)'s in each diagonal

$$

% Triangle Table

\begin{array}{c|cccc}

& j=1 & j=2 & j=3 & j=4 \ \hline

j=1 & L & \bbox[#B4B4FF, 2pt]{S} & \bbox[#FFFFC8, 2pt]{L} & \bbox[#B4F0B4, 2pt]{} \

j=2 & \bbox[#B4B4FF, 2pt]{L} & \bbox[#FFFFC8, 2pt]{} & \bbox[#B4F0B4, 2pt]{S} & \

j=3 & \bbox[#FFFFC8, 2pt]{S} & \bbox[#B4F0B4, 2pt]{L} & & \

j=4 & \bbox[#B4F0B4, 2pt]{S} & & & \

\end{array}

% Summary Table

\begin{array}{c|cc}

j & S_j & L_j \ \hline

2 & \bbox[#B4B4FF, 2pt]{1} & \bbox[#B4B4FF, 2pt]{1} \

3 & \bbox[#FFFFC8, 2pt]{1} & \bbox[#FFFFC8, 2pt]{1} \

4 & \bbox[#B4F0B4, 2pt]{2} & \bbox[#B4F0B4, 2pt]{1} \

\end{array}

$$

- Step 4 (Znm) → "Zanam"

- \(Z_{j} = \min(L_{j},S_{j})\) → Minimum

- \(n_{j} = L_{j}+S_{j}\) → Addition

- \(m_{j} =\text{rounddown}((n-1)/2,0)\)

- \(Z = \sum Z_{j}\)

- Step 5

- \(E(Z_{j})=\dfrac{n}{2}-\binom{n-1}{m}\times \dfrac{n}{2^n}\)

- \(V(Z_{j})=\dfrac{n(n-1)}{4}-\binom{n-1}{m} \dfrac{n(n-1)}{2^n} + E(Z_{j}) - E(Z_{j})^{2}\)

Then do hypothesis testing using this mean and variance. Just check if \(Z=0\) appears in the 95% confidence interval (select \(97.5\)-th percentile since it is a symmetric interval)

Residual Plot Test (#3)¶

-

Plot the weighted residuals against \(C_{ik}\)

-

(CONSTANT VAR) \(\propto 1\) → wtd. residual = \(C_{i,k+1} - C_{ik}f_{k}\)

- (VAR PROP TO LOSS) \(\propto C_{ik}\) → wtd. residual = \(\dfrac{C_{i,k+1} - C_{ik}f_{k}}{\sqrt{ C_{ik} }}\)

- (VAR PROP TO LOSS\(^{2}\)) \(\propto C_{ik}^{2}\) → wtd. residual = \(\dfrac{C_{i,k+1} - C_{ik}f_{k}}{C_{ik}}\)

Confidence Interval / MSE calculation¶

| Deviation | ||||

|---|---|---|---|---|

| \((\text{act}-\text{exp})^{2}\) | k = 1 | k = 2 | k = 3 | k = 4 |

| i=1 | 0.000 | 0.003 | 0.000 | 0.000 |

| i=2 | 0.029 | 0.001 | 0.000 | |

| i=3 | 0.003 | 0.002 | ||

| i=4 | 0.003 |

Honestly, \(k=1\) is not required. But may be required for \(\alpha_{k}^{2}\) calculation

Master Table¶

| k | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| alpha^2 | 4.46 | 2.24 | 0.00 | 0.00 | |

| alpha^2/f^2 | 2.37 | 1.52 | 0.00 | 0.00 | |

| dev i=4 | 765.00 | 928.79 | 1,123.72 | 1,172.58 | |

| inv sum | 0.00181 | 0.00169 | 0.00176 | 0.00169 | |

| se(R)^2 | 3,777.84 | ||||

| Reserves | 407.58 |

- \(\alpha^{2} = \dfrac{1}{(I-k-1)}\times \sum \prod(C_{k},\text{Deviations})\)

- inv sum = \(\dfrac{1}{\text{Dev}}+ \dfrac{1}{\sum(\text{Col except Diagonal})}\)

- \(se(R)^{2}=\text{Ult}^{2} \sum \prod(\dfrac{\alpha^{2}}{f^{2}},\text{inv sum})\)

Interval Calculation¶

Since the reserves are following a log-normal distribution, the confidence interval can be found out like so:

- \(\sigma^{2}_{i} = \ln(1+ \dfrac{se(R_{i})^{2}}{R_{i}^{2}})\)

- CI = \(R_{i} \times \exp(-\dfrac{\sigma^{2}_{i}}{2 }\pm z\sigma_{i})\)

Muffs¶

- Please read the entire question:

- On the top line one assumption was already given

- You were asked in (b) to give the other two. So, naturally you shouldn't state the one that was already mentioned before.

-

Implicit assumption: Development factors are not correlated ↩