Claims-made¶

Protip

Honestly, you just have to work with many problems related to claims-made to get a hang of it. No amount of reading will help you as much.

Understanding¶

- Retroactive date

- Nose coverage

- Tail coverage: Extended reporting endorsement

Gaps in Coverage¶

- Professional switch: Occurrence \(\to\) CM

- No gap as long as Occurrence expiry = Retroactive date

- Professional switch: CM \(\to\) Occurrence

- Gap since claims occurred in CM will not be covered post expiration.

- So buy tail coverage that overlaps with the Occurrence

- Professional retires:

- Same situation

- Buy tail coverage

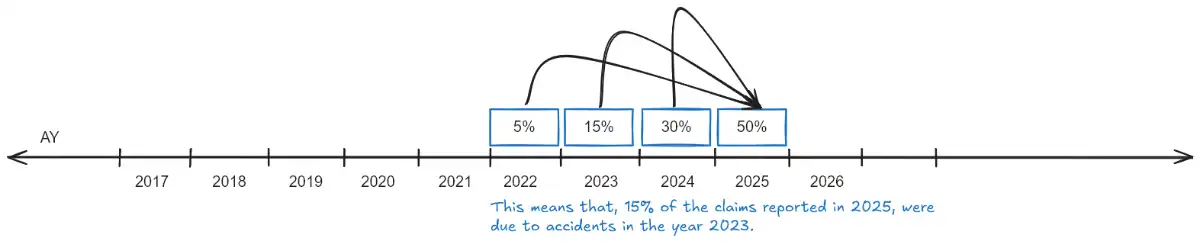

Report year organization¶

You can make Report year development triangles as usual to know development in claims made policies.

- RL = Report Lag

- L(Reported in year, Report Lag)

| RY | RL 1 | RL 2 | RL 3 | RL 4 |

|---|---|---|---|---|

| 2011 | L(2011,0) | L(2011,1) | L(2011, 2) | L(2011,3) |

| 2012 | L(2012,1) | |||

| 2013 | L(2013,2) | |||

| 2014 | L(2014,3) |

- The diagonal will be covered by Occurrence policy for AY2011

- SIMPLE MENTAL MODEL

- Think of a \(L(2012,1)\) as the accident occurred in 2012 - 1 = 2011, and was reported in 2012.

Principles of Claims-Made Pricing¶

P1: Price of CM vs Occurrence¶

- Price of claims made policies \(\lt\) occurrence policies, as long as costs are increasing

- More the time till settlement, more the cost of claims

- Occurrence has report lag + settlement lag

- CM has no report lag beyond the expiry of policy1

P2: Unpredictable change in underlying trends¶

- Occurrence covers claims reported in future years, more time for trends to impact the cost of those claims than for claims-made policies.

- Answer why claims made rates are more accurate and responsive.

- shorter forecast period for trends

- trends are uncertain, applying to shorter periods reduce uncertainty \(\implies\) accurate

- trend selections updated sooner because of shorter forecast period. \(\implies\) responsive

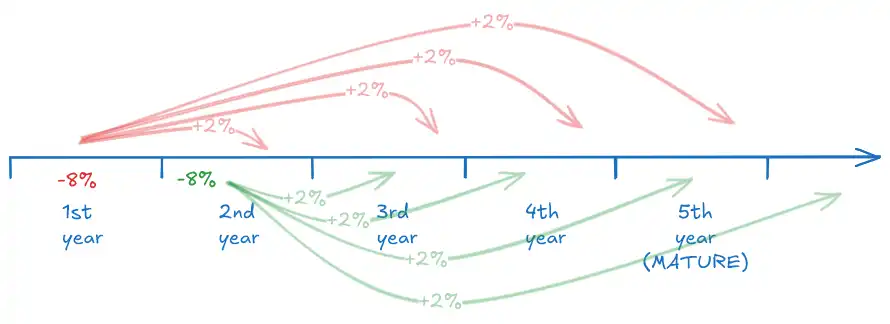

P3: Unexpected shifts in reporting patterns¶

If there is a sudden unexpected shift in the reporting pattern, cost of a mature claims-made policy will be affected relatively little, if at all, relative to an occurrence policy.

- Assume the reporting pattern changes, 8% less reported from each year

- -8% in the year (say, 1st year)

- 2% of those unreported claims are reported in the next (2nd year) 🤖

- 2% in the year after (3rd year) ⚒️

- 2% (4th year)

- 2% (5th year)

- This distribution is shown by the red lines

- The same happens for the 2nd year,

- -8% distributed in the next years (green lines)

- +2% (from 🤖)

- So net change in reporting in the 2nd year = -6%, not as much as the first year

- The same happens for the 3rd year

- -8% distributed in the next years (as shown in the previous years)

- +2% (from ⚒️ in first year)

- +2% from the 2nd year

- So net change in reporting in the 3rd year = -4%

- Continue with this trend…

- In the 5th year

- -8%

- But +8% from all the previous years…

- net change = 0%

Reiterating it, if there is a sudden unexpected shift in the reporting pattern, cost of a mature claims-made policy will be affected relatively little, if at all, relative to an occurrence policy.

P4: No liability for pure IBNR, risk of reserve inadequacy is reduced greatly¶

- CM only covered claims reported by the end of the policy term, don't have pure IBNR

P5: Investment income earned in CM is substantially less¶

compared to occurrence policies

- No report lag beyond the end of the policy term1

- less time than with occurrence policies for the premiums collected to be invested before claims are paid