Other Considerations¶

Regulatory Constraints¶

- Examples of rate regulation

- Examples of responses by companies

Operational Constraints¶

- Two examples

- Simple cost-benefit analysis

Marketing Constraints¶

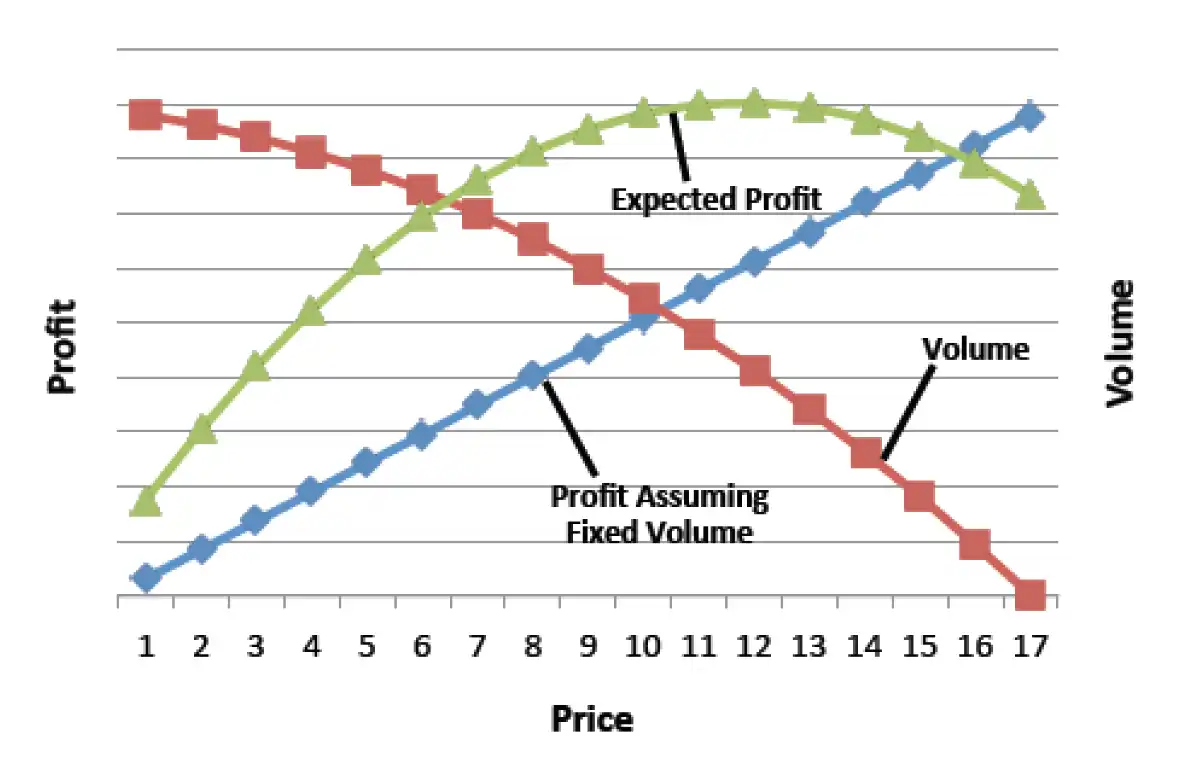

- Relationship between

- Blue = Profit based on price charged. For a fixed indicated cost per policy, they are directly proportional (also assuming volume is fixed)

- Red = Volume = # of insureds willing to buy coverage at each price. (Demand is inversely proportional to price)

- Green = Total expected profit, based on profit per policy and # of policies sold

- Factors influencing purchase decision

- Competitor's price

- Overall cost

- For Existing customers, rate changes

- Customer satisfaction & Brand Loyalty

Traditional Techniques for Mark Considerations¶

I am the insurer. CDPD

- Competitive: my policies, his rates

- Distributional: 30% in state, 10% in book (grow/shrink by segment)

- Policyholder Dislocation: change on retention

- Competitive comparisons

- Obtain competitor rates

- re-rate existing policies with my proposed & competitor's rates

- Analyze if you are cheaper than competitor or certain segments of this market.

- Challenges

- Difficult to get Competitor's rates

- Competitor's UW guidelines unknown

- Distributional analysis

- Identify which segments of book is growing/shrinking with time

- How my market share varies by segment of book

- e.g. if 30% drivers in state are 20-25 aged

- but we have insured only 10% of those drivers

- under-represented in the segment of market

- Policyholder dislocation analysis

- Impact of rate changes on existing customers

- Quantify the distribution of rate changes (% or $ amounts)

- Because customers with large changes are expected to have a lower probability of retention.

- ACTION: Pro-active action, prep the customer for the increase. Try to retain ("You can perhaps increase the deductible to offset the rate increase")

Systematic Techniques¶

Lifetime Value (renewal probability, long-term profitability)

Optimized Pricing (price elasticity of new vs existing customers)

Insurers try incorporating marketing considerations in pricing decisions directly. E.g. Lifetime Value Analysis (Asset Share Pricing) & Optimized Pricing.

- Lifetime Value Analysis

- Probability of an insured over entire lifetime (assumption about renewal probability)

- Expected Profitability over time

- e.g. Benefit of writing young drivers at a loss in the short-term, and as customers when profitability improves

- Optimized pricing

- Multivariate techniques \(\to\) price elasticity of new & renewal customers based on their characteristics.

- Price elasticity \(\to\) impact of rate change on close ratios & retention ratios.

- New customers are more sensitive to price.

- Existing customers, more friction (effort): shop for insurance and change carriers.

- Test different scenarios of rate changes: how it will impact total profit and growth

Underwriting cycle¶

"Hard" \(\to\) "Soft" \(\to\) "Hard"

graph LR

A["

**Hard Market**

---

*State:*

- High Prices & Premiums

- High Insurer Profits

*Result:*

- Low Growth (as high prices deter customers)

"]

B["

**Soft Market**

---

*State:*

- Low Prices & Premiums

- High Growth (as business is easier to write)

*Result:*

- Low or Negative Profits (due to price wars)

"]

A --

"**Action**: Insurers lower rates to gain market share

Reason: *Attract business with high profit margins*"

--> B

B --

"**Action**: Insurers raise prices & restrict underwriting

Reason: *Unsustainable low/negative profit levels*"

--> A

style A fill:#ffcccc,stroke:#b30000,stroke-width:2px

style B fill:#cceeff,stroke:#005c99,stroke-width:2px- Profit & Growth tends to be cyclical in nature

Arbitrarily starting from the hard market

- A "hard" market:

- prices and profits are high

- High prices so, growth is low

- To attract more business at high profit levels, lower rates.

- Urgently, all insureds lower rates to maintain competitiveness.

- Price competitiveness drives down profits for all insurers, what we call a "soft" market

- Prices are low, growth is high.

- Since profits are low or negative, to increase profitability, restrict writing of business.

- Eventually, all insurers raise prices \(\implies\) "hard" market