Cyclicity and test for Stationarity¶

- Cyclical variations

- gradual, long-term, up-and-down irregular repetitive movements

- rise and fall are not of fixed frequency

- period usually extends beyond a single year

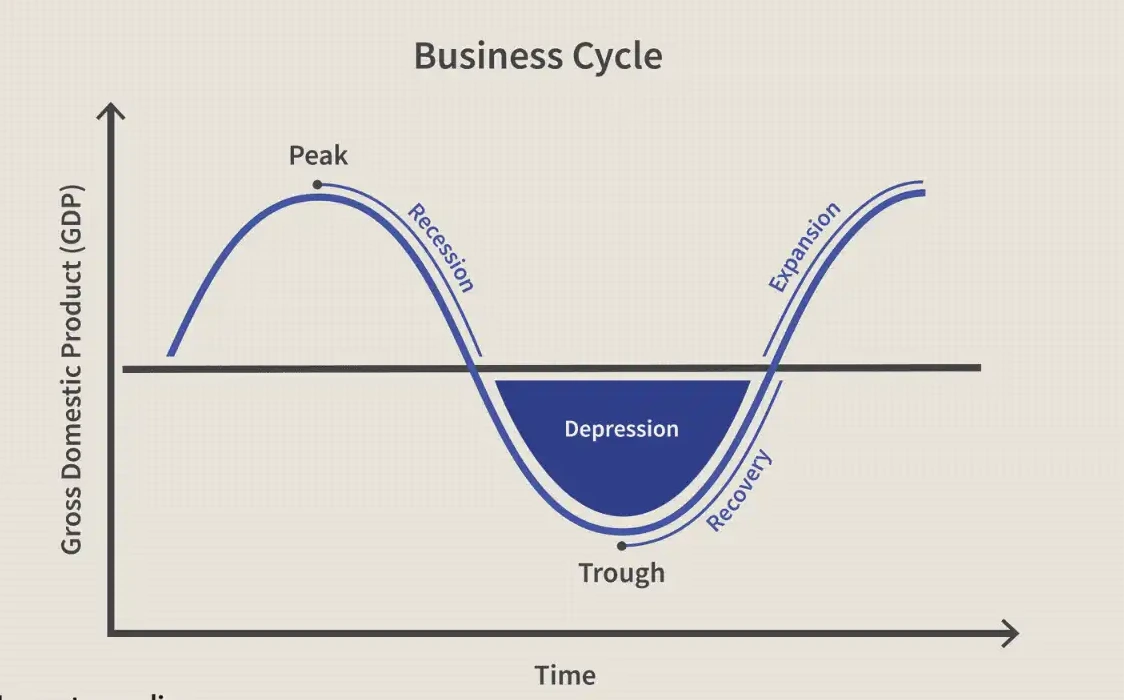

- 6 phases (Business Cycle)

- Expansion

- Peak

- Recession

- Depression

- Trough

- Recovery

- Examples

- Business cycle

- Price cycle : production decision

- Solar cycle: Sun's magnetic field (every 11 years, Sun's north and south poles shift entirely)

| Seasonality | Cyclicality |

|---|---|

| Calendar Efffects | Fluctuations not of fixed frequency |

| Average length is smaller | |

| Magnitude of cycles are higher |

Unit Roots¶

\[

Y_{t} - 1.9 Y_{t-1} + 0.9 Y_{t-2} = e_{t} - 0.5 e_{t-1}

\]

can be REwritten as

\[

(1- 1.9B + 0.9B^{2}) Y_{t}

\]

The roots of this equation are \(1\) and \(\dfrac{10}{9}\). Thus, this model has a unit (1) root.

Unit roots make the process non-stationary.

But why?

Difference once: \(W_{t} = \nabla Y_{t}\)

\[

w_{t} - 0.9 w_{t-1} = e_{t} - 0.5e_{t-1}

\]

which is a stationary ARMA(1,1). Thus the original model is ARIMA(1,1,1) which is non-stationary.

Why is Unit Root a problem?

Unit roots imply that the model structure is \((1-B)Y_{t} = Y_{t} - Y_{t-1}= f(e_{t})\), implying that the current value is same as the past value plus some function of random errors. Thus, our model will never converge to a mean.

- Causes of Non-stationary

- Unit roots present

- Deterministic polynomial trend present (\(+b\) exact structure can be determined)

- Stochastic trend present (\(+bt\) exact structure cannot be determined, time dependent.)

Tests of Stationarity¶

Augmented Dicky Fuller (ADF) Test¶

Is a unit root present?

\[

\begin{matrix}

H_{0}: & \text{series is non-stationary} \\

H_{\alpha}: & \text{series is stationary}

\end{matrix}

\]

Kwiatkowski-Phillips-Schmidt-Shin (KPSS) Test¶

Is there a deterministic trend (or mean)?

\[

\begin{matrix}

H_{0}: & \text{series is stationary} \\

H_{\alpha}: & \text{series is non-stationary}

\end{matrix}

\]

Phillips-Perron (PP) Test¶

Goal and Hypothesis setup same as #Augmented Dicky Fuller (ADF) Test

- Different assumptions about error terms

- More robust in the presence of

- autocorrelation

- heteroskedasticity

Variance Ratio Test¶

Test for random walk.

\[

\begin{matrix}

H_{0}: & \text{series is non-stationary} \\

H_{\alpha}: & \text{series is stationary}

\end{matrix}

\]

- Ratio significantly different from \(1\) \(\implies\) Not a random walk