Lecture 26 The Value Function

- The Value function

- Carrier of value = change in wealth or welfare1

- e.g. our response to attributes like brightness, loudness or temperature, past experience contexts, defines an adaptation level or reference point

- An object is felt based on the feeling one has already adapted to.2

- Same principle applies to non-sensory attributes like health, prestige and wealth

- Strictly: value = \(f(\text{Asset position},\text{Change})\)

- However, preference order is not altered by variation in asset position

- Certainty equivalent of \((1000,0.5)\) lies between \(300\) and \(400\) (when it should have been \(500\)) in a wide range of asset positions.

- \(\implies\) Approximation: ignore the asset position and only take change, will give a satisfactory approximation.

- Many sensory and perceptual dimensions share:

- psychological response is a concave function of magnitude of physical change3

- e.g. \(3\degree\) vs \(6\degree\) is easier to discriminate than \(13\degree\) vs \(16\degree\)

- Similarly

- Difference in gain of \(100\) vs \(200\) appears to be significant when compared to \(1100\) vs \(1200\)

- And difference in loss of \(100\) vs \(200\) appears to be significant when compared to loss of \(1100\) vs \(1200\) unless the larger loss is intolerable

- \(\implies\) Value function for changes in wealth

- concave above reference point (\(v''(x) \lt 0\) for \(x\gt 0\))

- convex below it (\(v''(x) \gt 0\) for \(x \lt 0\))

- Marginal value of gains and loss generally decreases with their magnitude

-

Value functions derived from risky choices shares the same characteristics

- Some #doubt In PT, are the outcomes mutually exclusive?

-

The following prospects, \(A\) vs \(B\) and \(C\) vs \(D\)

| Gamble | Prospect | Votes|

| ------ | ---------------------------- | ---- |

| A | \((6000,0.25)\) | 18% |

| B | \((4000, 0.25; 2000, 0.25)\) | 82% |

| C | \((-6000, 0.25)\) | 70% |

| D | \((-4000, 0.25, -2000, 0.25)\) | 30% | -

\(\pi(0.25)v(6000) \lt\) \(\pi(0.25)[v(4000) + v(2000)]\)

- \(\pi(0.25)v(-6000) \gt\) \(\pi(0.25)[v(-4000) + v(-2000)]\)

- So, \(v(6000) \lt v(4000) + v(2000)\) (Concave)

- And \(v(-6000) \gt v(-4000) + v(-2000)\) (Convex)

- Utility function should leave room for special circumstances' effects on preferences

- Person who needs \(\$60,000\) to buy a house, will reveal an exceptionally steep rise in utility near the critical value.

- Similarly, aversion to losses may increase sharply near the loss that is intolerable (compels him to sell his house)

- \(\implies\) Derived value function of an individual doesn't reflect "pure attitudes to money" (as it is affected by additional consequences)

- These create convex regions in value for gains and concave regions in value for losses

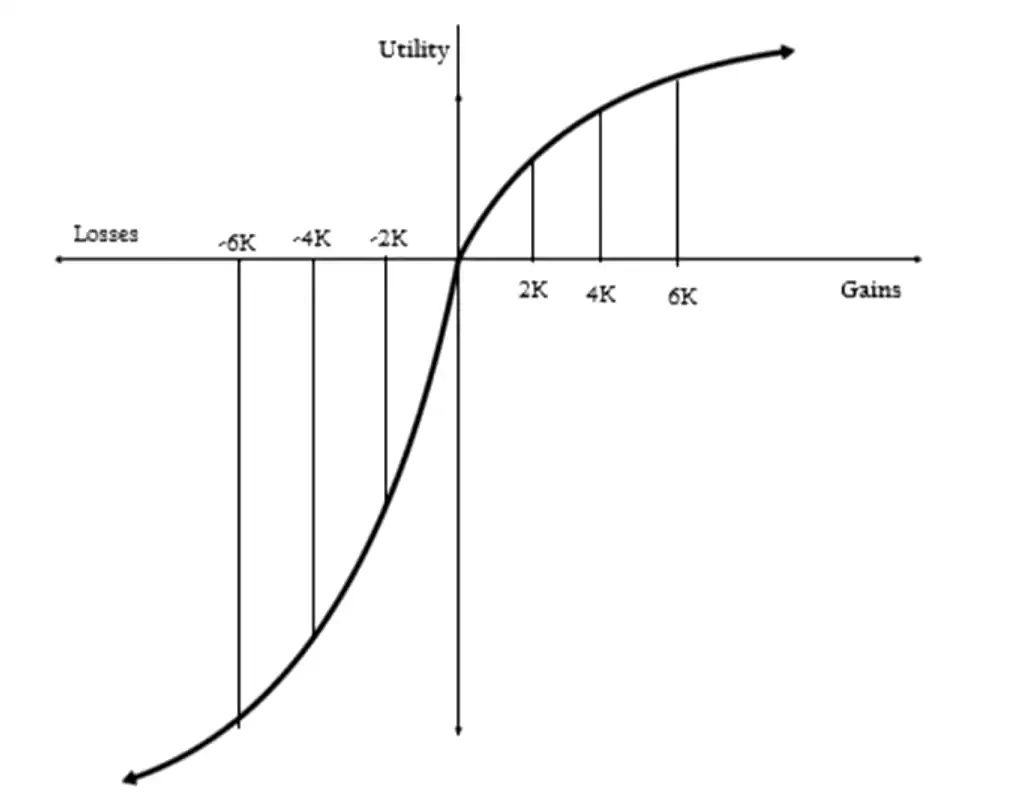

- K&T propose that Value function is

- Defined on deviations from reference point; \(0\) is the reference point in this case (perceived gains and losses)

- concave \(\to\) gains. convex \(\to\) losses4

- steeper for losses than for gains5

- If \(x \gt y \gt 0\) (proof for (3))

- \(\implies v(y) + v(-y) \gt v(x) + v(-x)\)

- For \(y=0,\) \(-v(-x) \gt v(x)\)

-

Let \(y\) approach \(x\) \(\to\) \(v'(-x) \gt v'(x)\)

- K&T focus on changes:

"Chances are the way Humans experience life"

- K&T focus on changes:

-

Say someone is earning 80000 and gets a 5000 bonus. According to Neoclassicals, it may not be a big amount as this is a one-time thing and when compared to the lifetime wealth expectancy, it is nothing.

- However, when she compares it to her current scenario, she says "Wow! An extra 5000!"

- Empirical Evidence

- Detailed analysis of von Neumann-Morgenstern utility functions for changes to wealth

- Functions obtained from 30 decision makers (5 independent studies)

- Observations

- most gains were concave

- most losses were convex

- only three individuals exhibited risk aversion for both gains and losses

- except one, utility was considerably steeper for losses than for gains

-

Consistent with the basic assumptions of perception or judgement ↩

-

E.g. Dip each of the hands in hot and cold water, and then dip both hands in the same lukewarm water. Both get a different sensation ↩

-

I.e. it is felt harder at extremes but not in intermediate points ↩

-

Diminishing marginal sensitivity \(\implies\) risk-aversion in gains, risk-seeking in losses ↩

-

Losses loom larger than gains. One experience from losing has a greater aggravation than the pleasure of gaining the same amount \(\implies\) most people find symmetric bets distinctly unattractive. aversiveness increases with the size of the stake. ↩