Lecture 25 Prospect Theory Evaluation

Sairam

- PT - Evaluation

- Once editing phase is done, evaluate each of the edited prospects, and choose the prospect with the highest value.

- \(V:\) Value function (overall value of edited prospect)

- expressed in terms of two scales

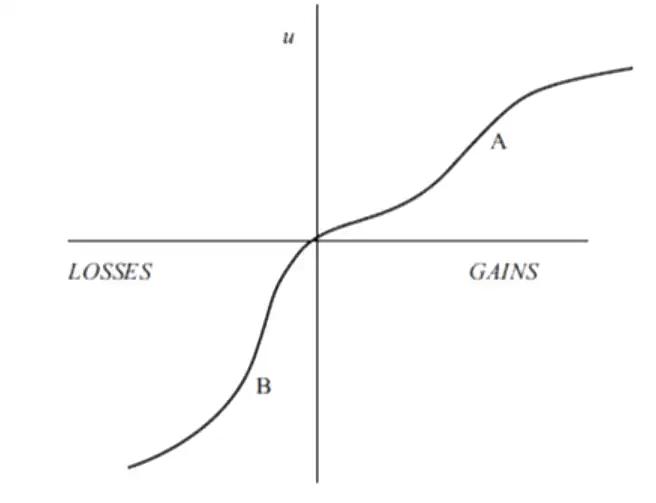

- \(v(x):\) assigns subjective value to each outcome \(x\). Deviations from the reference point (gains/losses)

- \(\pi(p):\) impact of probability \(p\) on overall value of prospect. Decision weight.1

- \((x,p;y,q)\)

- \(\implies\) \((x,p;y,q;0,1-p-q)\).

- Prospect is strictly positive if \(x,y \gt 0\) and \(p+q = 1\) (i.e. all outcomes are positive) and strictly negative if all outcomes are negative.

- regular if neither strictly positive nor strictly negative

- Corner example: \((400,0.4; 200, 0.5)\)2

- If \((x,p;y,q)\) is regular

- \(V(x,p;y,q)\) = \(\pi(p)v(x) + \pi(q)v(y)\)

- where \(v(0)=0,\ \pi(0)= 0,\ \pi(1) = 1\)

- \(V\) defined on prospects. \(v\) defined on outcomes

- \(V(x,1.0) = V(x) = v(x)\) for sure/certain prospects

- Generalization of \(EUT\) by relaxing expectation principle

- Situation (coin toss) for a regular prospect

- Heads: gain $20

- Tails: lose $10

- \(V(20,0.5;-10,0.5)=\) \(\pi(0.5)v(20) + \pi(0.5)v(-10)\)

- Rules for strictly positive/negative prospects

- Riskless Component (min gain/loss which is certain to be obtained)

- Risky Component (additional gain/loss which is actually at stake)

- Evaluation: If \(p+q = 1\) and \(x \gt y \gt 0\) or \(x \lt y \lt 0\)3

- \(\implies\) \(V(x,p;y,q) =\) \(v(y) + \pi(p)[v(x) - v(y)]\)

- \(=\) riskless component + value-difference between outcomes \(\times\) weight associated with more extreme outcome (here \(x\))

- Essential feature: decision weight is applied to the risky component \(v(x) - v(y)\) and not the riskless component \(v(y)\)

- Markowitz #economist was the first one to propose, "Utility should be defined to gains and losses rather than on final asset positions..."

- Proposed utility function which has concave and convex regions in both +ve and -ve domains

- Many attempts were made to replace probabilities with more general weights. So that we have a perception of risk rather than the outcome's probability directly. To explain aversion for ambiguity.4

- Effects of reference point are accounted for by assuming that values are attached to changes rather than final states. (hence a different rule for strictly positive/negative prospects )

- Anomalies of preferences implied by PT are expected to occur and can be used by the decision-maker, who cannot rely on expected utility theory henceforth.

-

NOTE: \(\pi\) is not a probability measure ↩

-

is not strictly positive because the probabilities don't add up to \(1\) meaning, there is a zero outcome possible. Making it not strictly positive. ↩

-

Strictly positive: \(y\) is smaller... so \(v(x) - v(y) \gt 0\). Strictly negative: again, y is the smaller loss. The one that is closer to zero is the smaller loss or gain. ↩

-

In expectation theory, we directly do a

sumproductof outcome values and their probabilities. (Rationally good) but in Prospect theory we do asumproductof perceived value (subjective) and decision weight of the probability. ↩